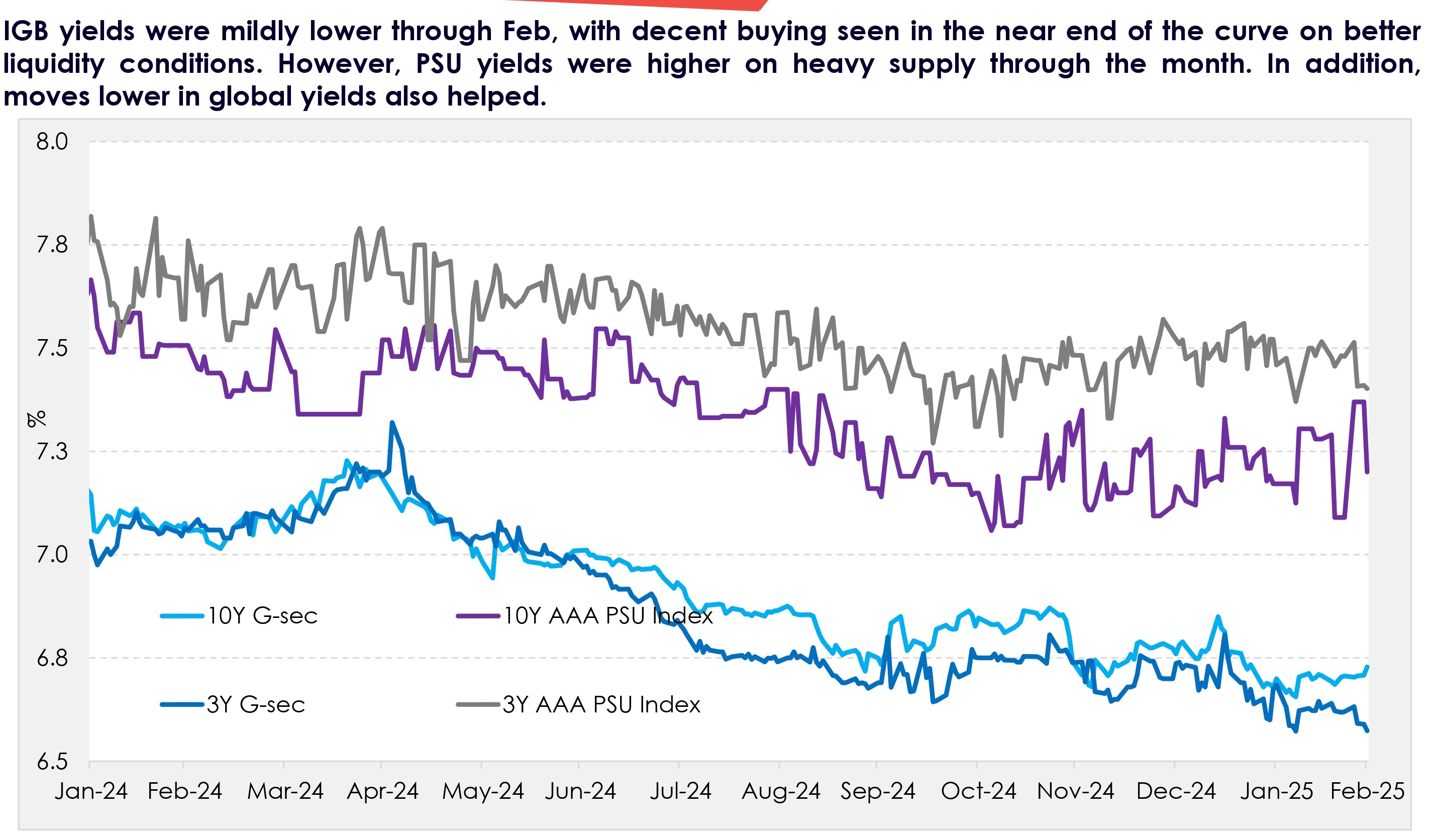

In this edition of Bond Compass, we highlight the key themes for Feb : • India G-sec yields edged lower in Feb, with more demand seen in the near end of the curve – aided by improvement in liquidity conditions. The RBI in Feb conducted a USD-INR buy-sell swap auction of INR 10bn – supporting durable liquidity. In addition, the central bank shall be conducting OMOs of INR 1tn (to be held in two equal tranches) as well as one more buy sell swap auction of USD 10bn in Mar. • India Q3 GVA growth came in at 6.22% YoY vs 5.81% previous – with higher positive contribution from agriculture, trade, hotels, transport and communication. The GDP growth also recovered, with an upward revision in Q2. Improvement in Oct-Dec GDP growth was led by both private and government consumption expenditure.