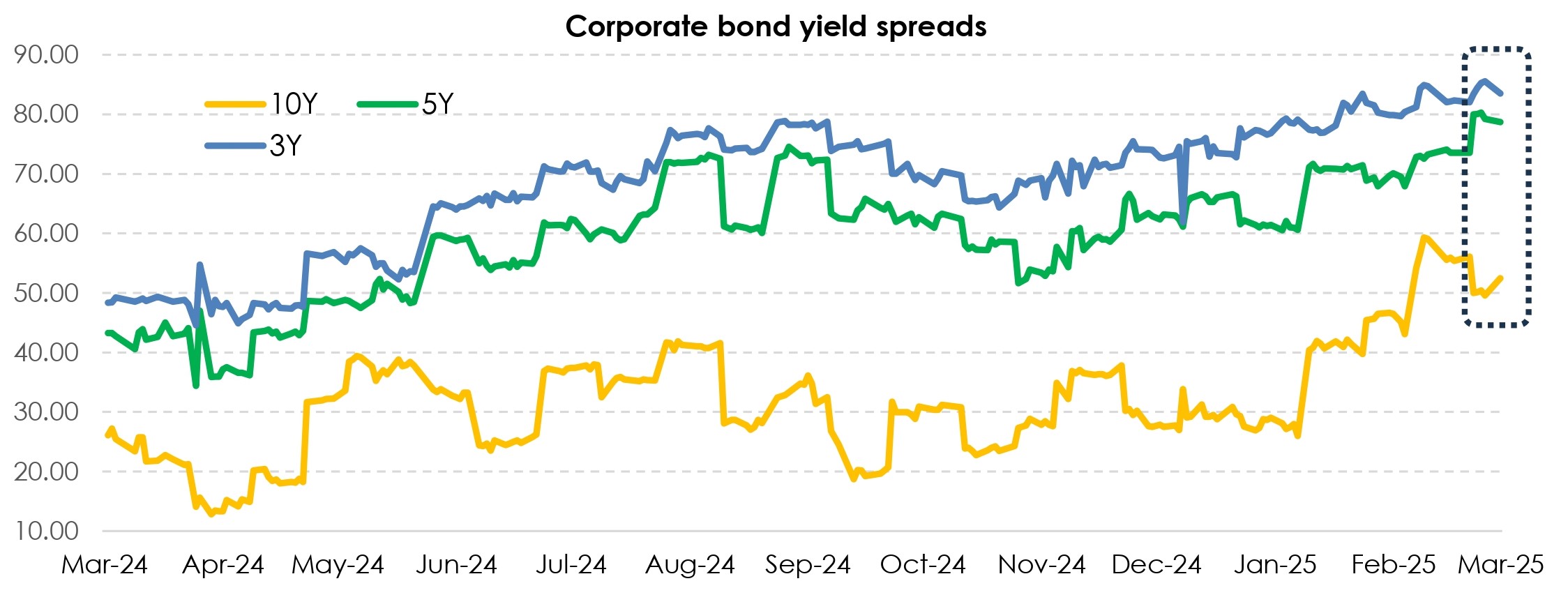

IN corporate bond spreads narrow with improvement in liquidity conditions, optimism around aggressive policy easing The most important metric for assessing risk perception in the bond market is the credit spread which is the difference between the yield of a corporate bond and comparable risk-free asset. Highly rated bonds (with ratings of AAA and AA) are traded relatively actively, and their yields reflect changing perceptions of investors regarding the riskiness of these bonds. Movement over time of credit spreads on corporate bonds is therefore a good indicator of the bond market’s perception of risk*. In this note, we look at the credit spreads of AAA rated bonds of 3Y, 5Y and 10Y maturities** over the past one year. In the first half of the financial year, yield spreads were mostly higher in line with tight liquidity conditions as well as limited prospects of near-term easing. The spreads continued higher going into H2 FY25 – this was on account of further tightening in domestic liquidity conditions (given active RBI intervention in spot markets to cap sharp depreciation in INR) along with heavy supply. The spreads peaked out in March and have shown signs of easing over the past few sessions this month. We expect spreads to narrow further going into March-end and then consolidate in the near term.