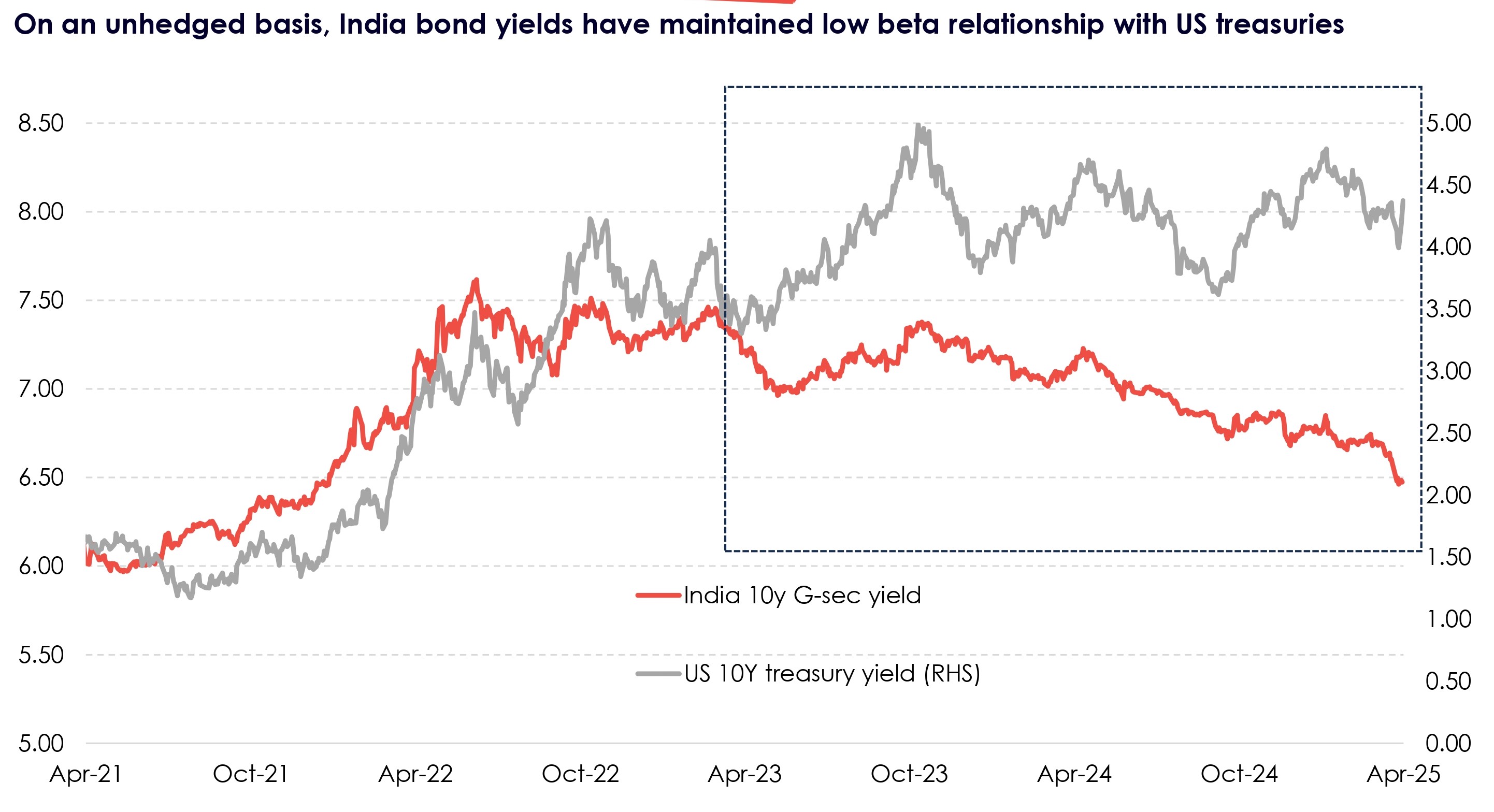

In this edition of Bond Compass, we highlight the key themes for Mar/Apr : • India G-sec yields came lower in March, with the momentum picking up in April. This was on account of sharp improvement in liquidity conditions as well as optimism around easing policy rates. In addition, softer than expected headline inflation reading also aided. • In the April MPC meeting, the committee unanimously cut rates by 25 bps, and shifted to an accommodative stance. This outcome was largely along expected lines, though governor’s remarks around ‘growth more of a concern than inflation’ helped sharp moves lower in yields. Market participants anticipate 50 bps further easing in policy rates this year. India FY26 growth and CPI inflation forecasts were revised 20 bps lower, with limited impact seen from US tariff announcements.