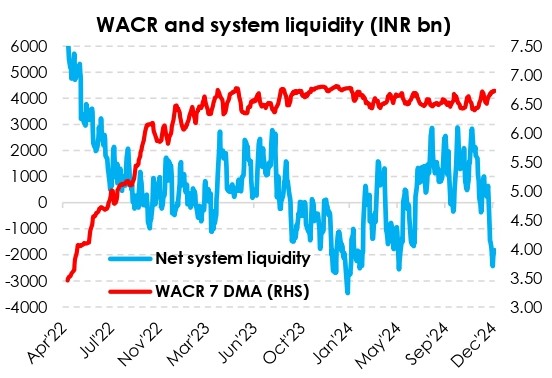

India liquidity deficit was the widest since May’24 following quarterly advance tax payments and GST outflows. Impact of these frictional outflows were accentuated by consistent RBI intervention in FX markets (taking durable liquidity out of the system). The RBI has continued to undertake a series of fine-tuning operations (variable rate repo auctions) to ensure that the weighted average call rate remains within the policy corridor (with SDF being the lower bound and MSF as the upper bound rate). As on 27th Dec, system liquidity deficit was at INR 1.83tn (without adjusting for daily CRR imbalances). Liquidity conditions will improve this week on the back month-end GOI spending as well as on flows emerging from the second tranche of 25 bps CRR cut (starting 28th Dec fortnight)