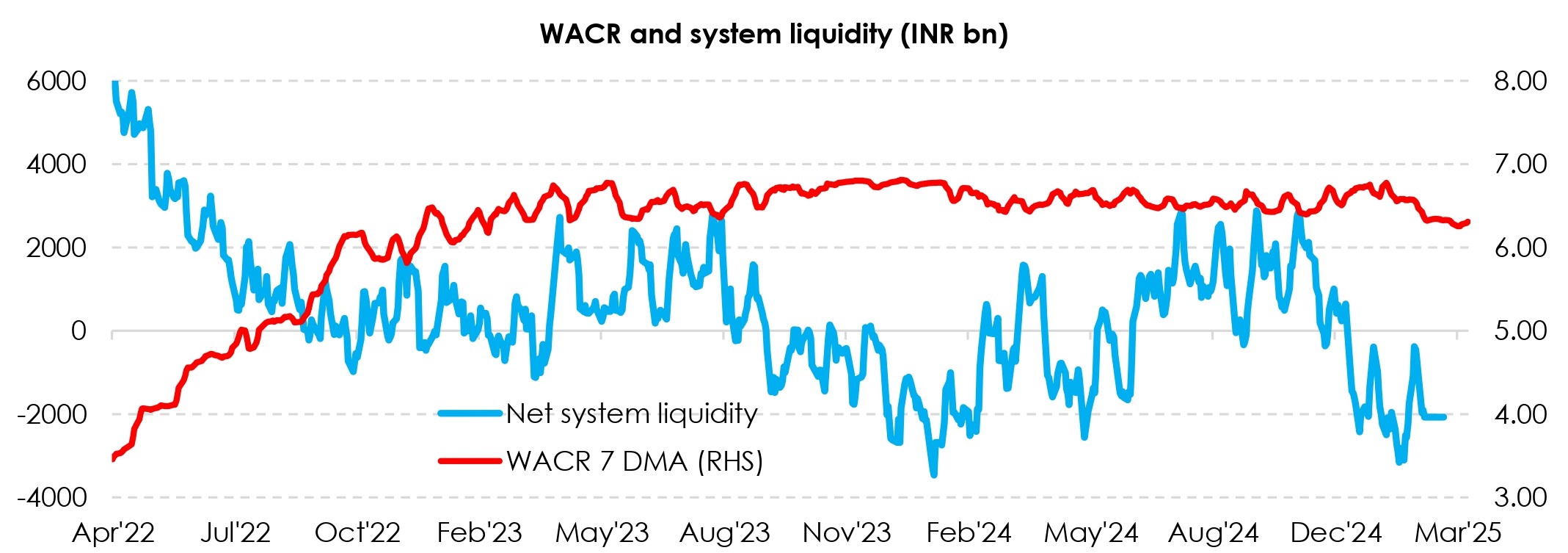

Liquidity Conditions set to improve following RBI’s durable measures, heavy month-end spending India system liquidity deficit widened to INR 2.6tn or -1.12% of net demand and time liabilities (NDTL) as on 18th Mar– following quarterly advance tax payments, with further tightening likely on the back of GST flows (that will happen between 19-20th Mar). However, conditions will likely improve on the back of INR 1tn OMOs of 500bn each along with a USD/INR buy-sell swap auction of USD 10bn on 24th March. (Note- Out of INR 1tn OMOs, one OMO auction of INR500bn was conducted on 18th Mar, and will get reflected in Thursday’s money market opearations release, and another OMO will be held on 25th Mar). Despite liquidity slipping into a deficit of over -1% of NDTL, the operating monetary policy target rate,i.e – weighted average call rate (WACR) has remained within the policy corridor (with SDF as the lower bound and MSF as the upper bound rate). This is likely on account of RBI’s continued fine tuning opeartions across overnight and term maturities. The appetite for term repo appears to have moderated, likely on pickup in OMO purchase auctions as well as on hopes of improvement in liquidity situation. Under term repos, the central bank has infused INR 2.45tn via 3-5 day VRRs, INR 4.36tn via 14-day VRRs, and INR 1.83tn via other long term repos so far in the ongoing quarter. In addition to the central bank’s injection of durable liquidity, conditions are set to improve likely on heavy month-end GOI spending (going by seasonal trends after a sharp rise in GOI cash balances).