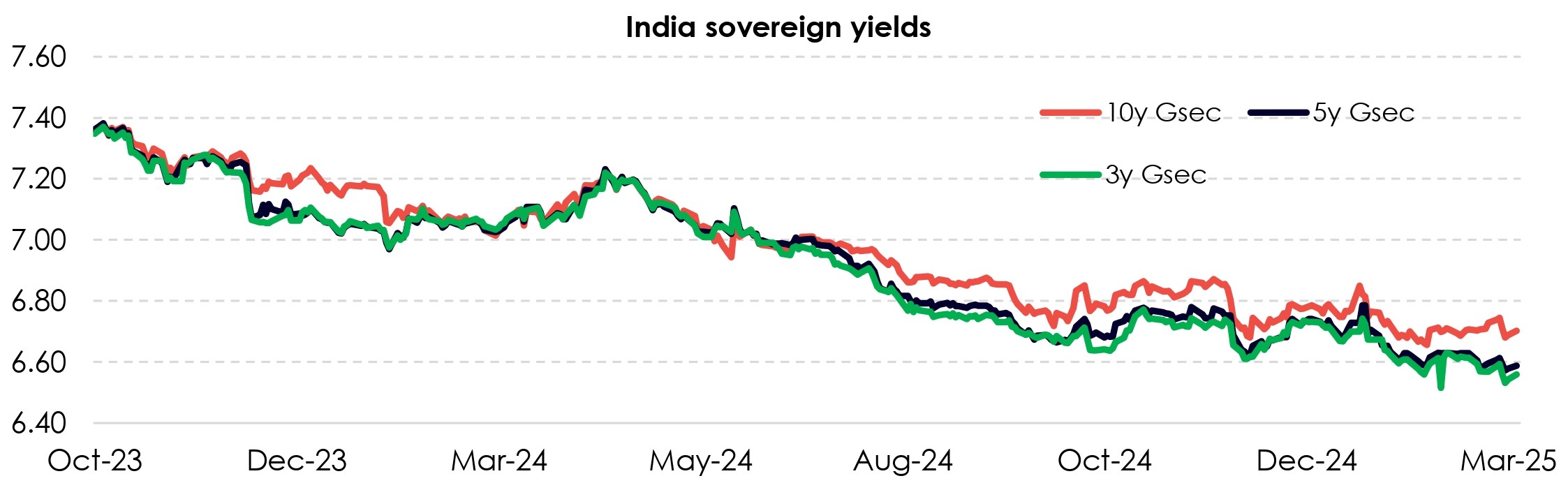

An update on India rates, liquidity and the path ahead India Sovereign yield curve has bull steepened in Mar – indicating that the near end of the curve has outperformed the duration segment. This is likely on account of an improvement in system liquidity conditions. The average liquidity deficit (without adjustments to daily CRR imbalances) stood at INR 820bn until 11th Mar (ahead of quarterly advance tax outflows) as against INR 1600bn in Feb. Conditions remained tight in Feb on anecdotes of RBI intervention in spot markets, with a selling of USD ~10-15bn heard, though this was partly offset by INR 800bn OMO purchase in the month. In addition, the RBI has also announced OMO purchase auction of INR 1tn – to be held in two equal tranches of INR 500bn (on 12th and 18th Mar) along with a buy-sell swap of USD 10bn on 24th Mar. These operations to inject durable liquidity will partly offset the impact of frictional tax outflows (both quarterly advance tax and monthly GST). Apart from these, the central bank has been conducting 2-way fine tuning operations – keeping the weighted average call rate within the policy corridor. We expect liquidity conditions to remain mildly in deficit through March, though conditions will start improving from the new FY, with pickup in government spending.